China's luxury market stabilises as watches remain under pressure

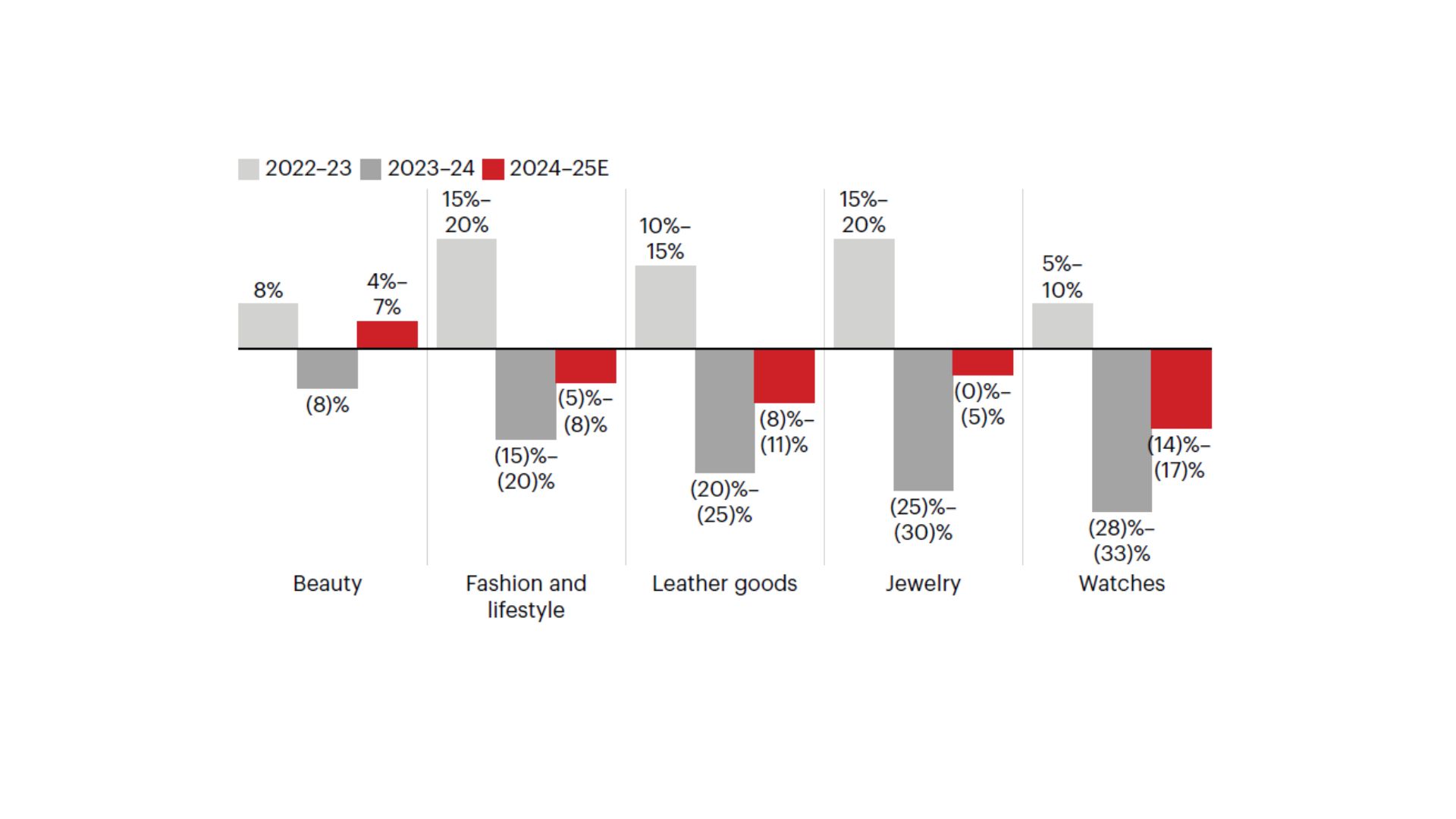

China's personal luxury goods market contracted by 3%–5% in 2025, showing a marked slowdown from the previous year's sharp decline. Although consumer confidence remained cautious for much of the year, early signs of recovery emerged in the second half, spurred by a stronger stock market and improving sentiment. The market is currently characterized as being in a recalibration phase, where consumers are becoming more selective and focused on value-driven luxury that balances quality, exclusivity, and practicality. Experience-led spending, such as travel and wellness, continued to outperform material purchases. Performance across categories was uneven, with beauty returning to growth driven by demand for ultra-premium skincare and fragrance. In contrast, watches faced significant pressure, with a projected decline of 14%–17%, as consumers shifted towards alternative investments and secondhand options. The secondhand luxury market grew by 15%–20%, highlighting its role as a complementary pillar in China's luxury ecosystem. Looking forward, modest growth in China's personal luxury market is anticipated for 2026, although performance will remain highly dependent on specific categories and brands amid ongoing volatility.